Latest research on the global EPOS market shows surge in activity as leading retailers refresh their point-of-sale technology

Accelerated store transformation initiatives boost US market

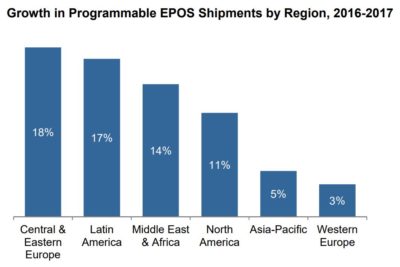

The programmable EPOS market grew by 8 percent in 2017, with shipments surpassing the 2.1 million mark for the first time, according to Global EPOS and Self-Checkout 2018, a new study by strategic research and consulting firm RBR.

US retailers invested heavily in EPOS upgrades as part of a wider focus on store transformation, particularly top-tier firms in the hospitality and service industries. Store openings by food and non-food discounters also contributed to drive a surge in deliveries.

Replacement projects by leading grocery retailers in western Europe and Japan continued – supermarket chains including Germany’s Lidl and Spain’s Mercadona are refreshing their hardware fleets, as are Japanese convenience store giants Family Mart and 7-Eleven.

Intense competition in China fuels shipments uplift

© Global EPOS and Self-Checkout 2018 (RBR)

After several years of slowing growth, EPOS sales picked up in China, boosted by new entrants to the already competitive market. Such firms have targeted small and medium businesses, offering products supporting mobile payment options such as Alipay and WeChat Pay, putting established players under price pressure.

Elsewhere in Asia, the development of emerging retail markets continued apace, with shipments up strongly in the Philippines and Vietnam.

Physical retail expansion drives expansion in a diverse range of markets

Store retailing remains in healthy shape across much of the world, with physical network expansion driving EPOS growth in countries as diverse as Mexico and the UAE. In India, shipment activity was up strongly, as the retail sector becomes increasingly open as a result of the ongoing relaxation of rules on foreign direct investment.

Although there are fewer opportunities for retailers to grow their store networks in central and eastern Europe (CEE), a large-scale upgrade project in Russia and fiscal regulation changes in Czechia caused a spike in EPOS shipments.

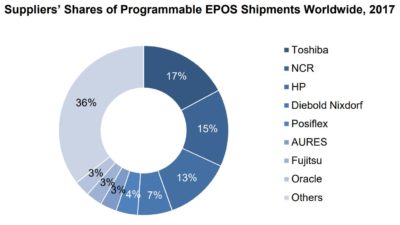

Toshiba remains the world’s largest EPOS vendor, but NCR and HP gain ground

© Global EPOS and Self-Checkout 2018 (RBR)

Toshiba is the largest EPOS vendor in the world, supplying 17 percent of shipments. The Japanese vendor leads in both Asia-Pacific and Latin America. NCR increased its share by two percentage points to 15 percent and is number one in North America. HP also gained share and delivered the most units to the Middle East and Africa.

Diebold Nixdorf maintained its global share at 7 percent, leading in both western Europe and CEE. Taiwan’s Posiflex and Japan’s Fujitsu both have a global presence, each delivering more than half of their shipments to countries outside Asia-Pacific.

The vast majority of French vendor AURES’ deployments are in Europe, while more than half of Oracle’s terminals were delivered to the USA. In what is a relatively fragmented sector, more than a third of the market is supplied by other EPOS hardware vendors each with less than a 3 percent share.

EPOS investment to continue as retailers strive for seamless checkout experience

The outlook for physical retail remains difficult in North America and Europe, where demand for point-of-sale technology is moderated by store closures in countries with high e-commerce sales. However, the challenge from online retailing highlights the need for increased investment in store transformation technologies such as mobile POS, self-service devices and EPOS hardware, in order to achieve a seamless checkout experience.

RBR forecasts the installed base of terminals will grow by 15 percent to reach 16.4 million by 2023, boosted by increasing modernization of the retail sector in emerging markets and the growing adoption of EPOS devices in smaller businesses.

Source: RBR